[First Time Buyer Edition]

Funding a home, mortgages, borrowing, loans.

People panic when they hear these buzzwords. Confusion and stress can set in. And that’s normal given that most have not gone through a home buying process before.

We’re here to help and we’ve broken down all of the main parts you need to understand when learning about mortgages. And we’ve made it simple.

A point to note – we are not a mortgage broker or a financial advisor. This means you need to get independent advice for your personal circumstances to move forward with a mortgage product.

But… because we are not a mortgage broker – we don’t have to push products to you to make a sale. We are one of very few people online who can give an unbiased view.

Back to basics – why do you need a mortgage?

Houses are expensive – really expensive. For many they are the largest purchase of your life.

House prices have been measured over time with the average worker’s annual income (or wages). Currently in the UK a home is on average 8 times higher than annual income (up from 5 times in 2002). It’s worth bearing in mind that this is 8 times your salary before tax.

So really if the house price was measured as a proportion of the pay you took home after tax deductions, the number would be higher than 8 years!

How are mortgages calculated?

The cost of your mortgage focuses on:

- If you are choosing a repayment mortgage or interest only mortgage.

- How many years you are borrowing the money for (Called the Mortgage Term)

- How much of the home is the mortgage covering (Called the Loan to Value Ratio)

- If you can demonstrate good overall management of your own money (Called your Credit Rating)

Types of Mortgages

Interest only mortgages:

There are mortgages where you only pay the interest on the loan. There is no repayment of the capital amount. This means that after 10, 20, 30 years of repaying you would still have not paid off any of the capital amount of the loan.

Interest only loans are much more common for property developers instead of people who want to live in their home. Developers will either want to rent a property out after buying it, or will complete a renovation and sell it on later – neither of which require owning the property outright at the end of the mortgage period.

Casey took out a 20 year mortgage on a property costing £120,000.

The mortgage interest rate was 3% fixed for the whole term of the loan.

Casey paid the interest on the loan (being 3% or £3,600 per year).

After 20 years worth of repayments (£3,600 x 20 = £72,000) the outstanding capital amount on the mortgage was £120,000.

Casey did not live in the property and rented it out to tenants. The rental income from the tenants was high enough to comfortable cover the monthly mortgage repayments.

As she had other living arrangements, was not aiming to own the property at a later date and the property had increased in value over 20 years, she was happy to have the mortgage balance outstanding at the end of the mortgage term and sold the property at the end to clear the debt.

Repayment Mortgages:

Repayment mortgages are far more common for first time buyers.

A repayment mortgage is made up of the following parts:

- Capital (sometimes called principal)

- Interest

Capital is the part of the mortgage you are paying back to get for yourself. Think of this as ‘the prize’ to eventually win. You keep it when it’s repaid.

Interest is part that the bank receives for giving you the money in the first place. You don’t get this back.

Because you are paying back some of the capital amount each month as well as interest, repayment mortgages are more expensive than interest only. But the benefit of paying the capital off with the interest is that after making all of the loan repayments you will own the property.

Free Checklist for Buyers

Become more focused on your house purchase

Feel more prepared when you go for a property viewing

Beat the competition!

Mortgage Term

This one is quite straight forward. Paying off your mortgage over a longer time period means you have more time to pay it.

This means that your monthly repayments would be lower for a mortgage covering 35 years than a mortgage covering 25 years.

But because you are borrowing money for a longer time, you will end up paying more interest on the mortgage. This does make sense – the lender is providing you with the funding for a longer period of time and this needs to be paid for.

A shorter mortgage repayment period will mean you pay less interest over the life of the mortgage, but the monthly repayments will be higher.

George is in the process of getting a repayment mortgage arranged for his new home.

He has spoken with a mortgage advisor and has been told his mortgage rate will be 3% for the loan period.

The purchase price is £250,000

If George went with a 30 year mortgage this would mean repayments of £1,264.

But if George went with a 20 year mortgage this would mean repayments of £924.

Assuming the interest rate stayed the same for the entire loan, George would pay over 50% more interest to the lender over the full life of the mortgage

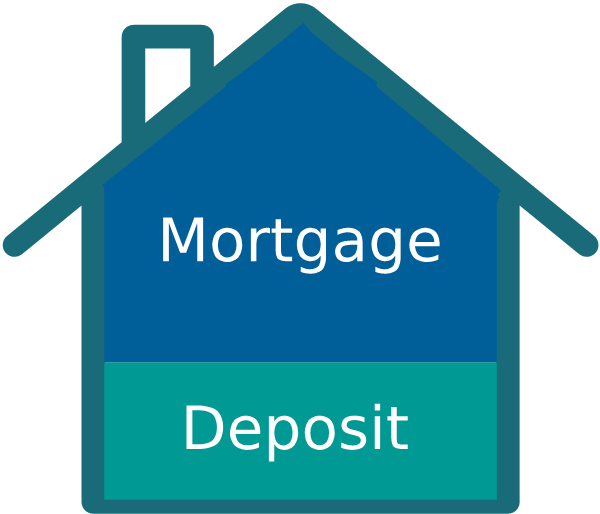

Loan to Value Ratio

The lender will want to look at three parts when working out this ratio.

-

- The size of your deposit that you are putting down

- The price you have agreed to buy the property from the seller

- The size of the loan (or mortgage) that is needed to pay the difference between your deposit and the price you agreed with the seller.

The lender will work out how big the loan is as a percentage of the property’s value.

If you a have a low deposit then the following happens:

Your mortgage needed to cover the repayments will be larger

The Loan to Value ratio will be higher

The rate of interest being charged will be higher

If you a have a high deposit then the following happens:

Your mortgage needed to cover the repayments will be lower

The Loan to Value ratio will be lower

The rate of interest being charged will be lower

Lenders charge in this way because it reflects the risk they are taking on. Consider an example of a first time buyer taking on a high mortgage that has a loan to value of 95%.

If the property price fell by more than 5% (like in a recession or difficult economic period) the value of the property would not be enough to cover what is owed by the lender. In other words, if you were unable to pay for the home and the lender had to sell it, they would make a loss.

The lender is taking on extra risk which results in charging you a higher rate of interest.

Unfortunately some lenders will even reject a loan application if the loan to value ratio is too high.

Credit Rating

Each person has their own credit rating, which is calculated by a credit rating agency. Lenders and other companies check your credit rating whenever they are about to extend you credit (e.g. if you were applying for a credit card, buying a car on finance or setting up a mobile phone contract.

If your credit rating is good you are likely to pass lender checks.

If your credit rating is poor your lender may still provide the mortgage to you, but the cost of the mortgage will be higher (a higher interest rate is likely to be charged). Some lenders may decide not to lend to you because of a low credit rating. So it’s important to keep track of your credit rating to see if there might be problems in the future.

How can I work out how much I can borrow?

Every lender will have different ways of working out how much to lend to you. Some will give you more, others will give you less.

Most lenders can give you a rough indication of how much they are prepared to lend to you. Most of them use a similar calculation. The calculation tends to run in the following way:

- They start with your monthly income payslip

- Take off any deductions/contributions that come out of your pay (like pensions, student loans, car schemes)

- Take off any repayments for other debts that you pay (like credit cards, personal loans, car repayments etc)

- Multiply your monthly income by 12 to get an annual income

Once the bank has calculated your ‘adjusted’ income – they will multiply it by their magic number (i.e. the income multiplier) to work out how much they are prepared to lend to you.

This is different for each bank and can also be different depending on what type of customer you are (in terms of how much you earn) and what type of mortgage you are going after.

Banks will not advertise these numbers everywhere and they can change suddenly. Most lenders will offer 4 times your annual salary. Some lenders will offer 4.5 – 5 times, and one lender is even offering 5.5 times.

Here are some of the links to the tools of the more popular lenders:

Barclays

Halifax

Santander

Lloyds

HSBC

Should I Get A Mortgage Broker?

Some people feel better in getting a mortgage broker to help them with the financial side of things.

Affordability

Brokers will discuss your requirements in more detail, running through your expenses and calculating your affordability.

Remember: Not all mortgage brokers charge you upfront for their work. Many are already paid a commission by the bank when you take out a mortgage, so you may not have to pay any upfront cost to them.

Deals

Sometimes mortgage brokers can get deals that are not available on price comparison websites – which is useful.

But by the same token, some independent brokers cannot offer the mortgages that banks provide directly to customers.

So – depending on the type of mortgage you are after, you might be better or worse off going to an independent broker instead of going direct to a lender and speaking to their mortgage advisor.

Lender Preference

Brokers also have useful knowledge into what type of customers and properties certain lenders prefer. This can save you valuable time in the process and reduces your chances of getting your application rejected.

For example, some lenders will allow you to borrow a higher amount when your salary goes past a certain level. Other lenders may not provide mortgages on flats that are above 4 storeys high. There are lots of different quirks between lenders, so it’s definitely not a ‘one size fits all’ policy.

Second Check

It’s also worth bearing in mind that brokers check the information you provide before the mortgage application is sent off. For some this can be a real help to avoid any errors in paperwork.

Even if you were to go directly to a lender for a mortgage, in most cases they are required to offer advice to you. Getting advice from a broker/mortgage advisor means that if the mortgage turns out to be unsuitable later on, you would have more rights if you made a complaint.

The Mortgage Approval Steps

Each lender can have a different process – but broadly speaking the following stages are below:

- Application is sent off to the lender – along with all the documentation you need to send off. They will carry out affordability checks and decide how much they are prepared to lend to you.

- Lender conducts a survey on the property. Usually this involves sending a surveyor out to look at the property – but sometimes this is done remotely (also called a ‘desktop review).

- Any concerns the lender has will be fed back to you (either through your broker or direct if you have not used one).

This could be valuation issues (off the back of the survey report) or legal concerns (to do with the property title and/or lease). - Mortgage Offer – fingers crossed the lender is happy and sends you an offer letter that states the conditions for giving you a mortgage.

*Note – this will normally require you to get buildings insurance for the property - Request Funds – When you are ready to complete the sale your solicitor will make the request to the bank for the funds to be sent through.

Rejected Applications

Sometimes a lender will highlight an issue they have with your mortgage application. Other times you may receive back a flat “no”.

There are many reasons why your loan application might be rejected. If this does happen the important thing is to concentrate on the feedback that comes back from the lender so that you can improve your application for next time.

It’s also worth using one of the free to use credit score apps to find out what is draggin your credit score down.

Icon Attributions: smalllikeart, freepik

Never Miss a tip!

Sign up to our mailing list and be the first to receive the latest information

Pingback: Why a 95% Mortgage is a Terrible Idea - Home Buying Tips

Pingback: Are New Builds Always Delayed? - Home Buying Tips

Pingback: How Do People Afford Houses? - Home Buying Tips